|

Secretaris-Generaal VN

Geregistreerd: 18 mei 2005

Locatie: Limburg

Berichten: 50.240

|

Een pronostiek voor morgenavond na beursslot?

Hier eentje:

Citaat:

https://seekingalpha.com/article/429...=mw_quote_news

Summary

Tesla's financial results will be announced Wednesday. One item of great interest always is Tesla's cash balance and particularly its change from the prior quarter.

With most loss estimates being a few hundred million dollars, unrestricted cash is likely to be little changed from the $5 billion reported at June 30, 2019.

The cash change is likely to be about $400 million better than the actual loss (or possible profit) for the quarter.

Non cash expenses and cash from asset liquidations are likely to be largely offset by investments and changes in debt levels.

A cash flow forecast, in an analytical format, is provided along with a discussion of the above referenced impacts.

Introduction

Based upon many comments and articles I have read on Seeking Alpha, there seems to be a great deal of confusion and misunderstanding regarding Tesla's (TSLA) ability to generate cash and what it means for the company. Many bears, particularly those of the TSLAQ variety, greatly underestimate Tesla's cash generating ability and overestimate its potential cash needs.

On the other hand, many of the bulls focus on "Operating Cash Flow" and "Free Cash Flow" incorrectly believing that if they are positive, it means that TSLA is creating value. This is not necessarily true for a few reasons. First of all, much of the positive operating cash flow is due to either paying employees in stock and stock options rather than cash or ongoing slow liquidation of the former SolarCity lease and loan portfolio. Positive Free Cash Flow doesn't necessarily mean much either, as it's calculated prior to principal payments on debt and payments to VIE investors. As a result, it's entirely possible to have positive Free Cash Flow but still see cash balances decrease.

Earlier this month, Tesla reported third quarter production and deliveries, which has caused many analysts to fine tune their estimates of the quarterly financial results to be reported Wednesday evening. The bulk of these estimates suggest a range from close to break even to as much as a $500 million loss, with some "outliers" in both directions. I'm not making any estimates of my own regarding the likely income or loss for the quarter, but instead have developed two cash flow scenarios based upon the likely range of results.

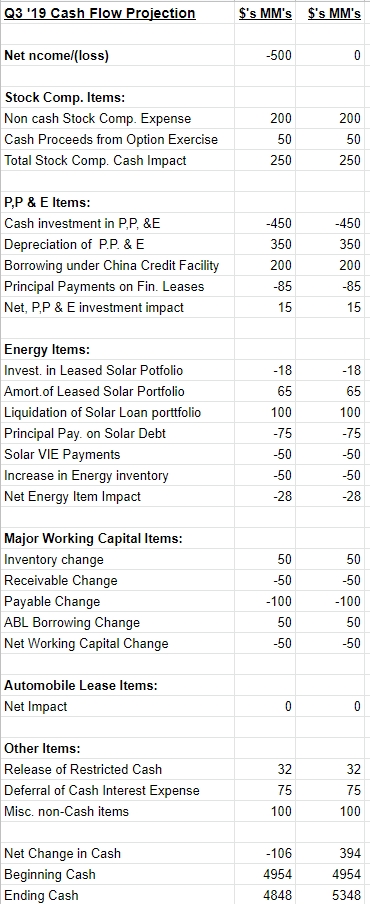

My Scenarios

In the two cash flow scenarios I have provided below, one assumes a $500 million loss, the other assumes the quarter is breakeven. The only difference in the scenarios is the net income/loss figure. Therefore, anyone who wants to "play along at home" can simply plug in their own estimated third quarter income (with ample opportunity to make other changes if they so desire).

In looking at the figures in the chart, the first thing to note is that I did not use the standard cash flow presentation of "Operating Cash Flow," "Investing Cash Flow," and "Financing Cash Flow." The standard presentation is important in large part simply because it's a standard format that analysts are familiar with, and, at least in a cursory review, provides a general "lay of the land." However, most readers who have reached this point in my article are likely well beyond the stage of simply trying to figure out the "lay of the land" for Tesla. As with many aspects of life, it's also valuable to look at things from different perspectives. My presentation format provides one of these perspectives. Where possible, I grouped cash flow items by topic or business line rather than its accounting category.

My scenarios are as follows:

...

Summary/Conclusions

The recently concluded quarter has been the most "normal" one Tesla has had in quite a while. There were no equity raises or significant new public debt issues. Furthermore, some of the kinks in the production and delivery process appear to be have been worked out, minimizing the likelihood of major operating cash flow swings this quarter due to those items.

As a result, this quarter may provide something of a "roadmap" for future quarters with respect to Tesla's ongoing cash flow situation. The most significant conclusion is that, barring special situations, Tesla's cash changes are likely to closely track and possibly be modestly better than its profit or loss each quarter. Cash generation due to liquidation of assets, particularly related to SolarCity, are to a large extent absorbed by required debt repayments, while investments in assets, whether it be for the China factory, inventory increases, or leased cars, can be offset by increased borrowing.

Finally, it should be noted that operating cash flow, taken out of context, is useless as a TSLA valuation tool.

Disclosure: I am/we are short TSLA. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

|

Laatst gewijzigd door Micele : 22 oktober 2019 om 13:13.

|